March 2015 Accounts HSC BOARD paper with solution

March 2015 Accounts Board Paper With Solution |

Q1. Attempt any THREE of the following sub - questions: [15]

(A) Answer the following questions in ‘one’ sentence each: [5]

1. What is ‘liability of partners’?

Ans. The ‘liability of partners’ are joint, several and unlimited as mentioned in ‘Indian Partnership Act - 1932’.

2. What is meant by ‘capital fund’?

Ans. Capital fund consists of contributions, entrance fees, surplus income, legacies and donations specifically received for capital fund.

3. What is ‘gain ratio’?

Ans. Proportion in which continuing partner gain the share of outgoing partner on his retirement.

4. What do you mean by ‘issue of shares at premium’?

Ans. Issue of shares at the value higher than their face value is known as ‘issue of shares at premium’.

5. What are ‘noting charges’?

Ans. Noting charges are the fees paid to the Notary public for recording the fact of dishonoured bill.

(B) Write a word / term / phrase which can substitute each of the following statements: [5]

1. Excess of income over expenditure of a ‘not for profit’ concern.

Ans. Surplus.

2. Debit balance of revaluation account.

Ans. Loss on revaluation .

3. The debentures which are convertible into shares.

Ans. Convertible debentures

4. A person who draws a bill of exchange.

Ans. Drawer

5. An asset which can be converted into cash immediately.

Ans. Liquid Asset.

(C) Select the most appropriate alternative from those given below and rewrite the statements: [5]

1. Dissolution expenses are credited to ___________ [Cash / Bank account]

a. Realisation account

b. Cash/ Bank account

c. Partners’ capital account

d. Partners’ loan account

2. Prepaid expenses are sown on the ____________ side of balance sheet. [Assets]

a. Assets

b. Liability

c. Debit

d. Cash

3. A bill is drawn on 23rd Sept, 2013 at 4 months would be payable on __________ [25th Jan. 2014]

a. 24th Jan. 2014

b. 25th Jan. 2014

c. 26th jan. 2014

d. 25th Jan. 2013

4. Capital Balance is ascertained by preparing ________________ [Statement of affairs]

a. Statement of affairs.

b. Cash account

c. Drawing account

d. Debtor’s account

5. From financial statement analysis the creditors are interested to know ________ [liquidity]

a. Liquidity

b. Profit

c. Share

d. Share capital

(D) State whether the following statements are True or False: [5]

1. Balance Sheet is a nominal account. [False]

2. Drawee can transfer the ownership of a bill. [False]

3. Debit balance of insolvent partner’s capital account is known as ‘capital deficiency’. [True]

4. A bill drawn in India and Payable in japan is a foreign bill. [True]

5. Under single entry system it is not possible to prepare trial balance. [True]

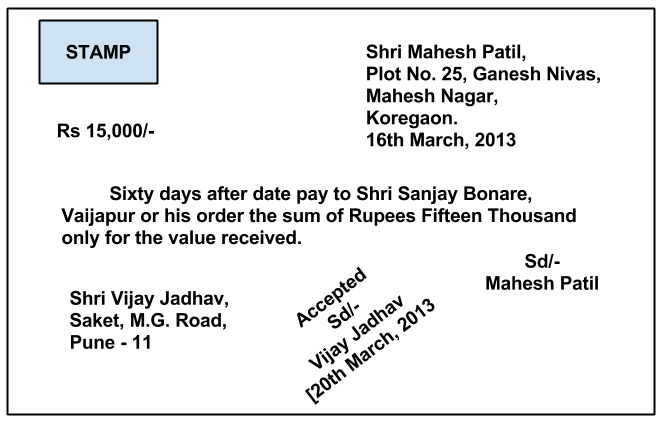

(E) Prepare a specimen of Bill of Exchange from the following information:

Drawer - Shri Mahesh Patil, Plot No. 25,, “Ganesh Nivas”, Mahesh Nagar, Koregaon.

Drawee - Shri Vijay Jadhav, “Saket” M.G. Road, Pune - 11

Payee - Shri Sanjay Bornare, Vaijapur.

Period of bill - 60 days.

Date of bil : 16th March, 2013

Amount of bill - ₹ 15000

Date of acceptance - 20th March, 2013.

Particulars | 01.04.2012 Amount (Rs.) | 31.03.2013 Amount (Rs.) |

Cash in hand | 10000 | 16000 |

Cash at bank | 20000 | 36000 |

Stock | 16000 | 24000 |

Furniture | 18000 | 18000 |

Plant and Machinery | 60000 | 90000 |

Creditors | 15000 | 18000 |

Debtors | 24000 | 30000 |

During the year Mr. Anil has withdrawn ₹ 10,000 for his private purpose and bought goods of ₹ 2000 for household use.

On 1st October 2012, he sold his household furniture for ₹ 2,000 and deposited the same amount in the business bank account.

Provide depreciation on Machinery @ 10% p.a. (assuming additions were made on 1st October, 2012) and on furniture @ 5%.

Prepare:

(a) Opening Statement of Affairs.

(b) Closing Statement of Affairs.

(c) Statement of Profit or Loss for the year ended 31st March 2013.

OR

(A) What are the components of current ratio? (4)

(B) State the objectives of financial statements from the viewpoint of a business concern. (4)

Q3. Akash and Suraj are partners in a firm sharing profits and losses in the ratio 3:2. Their balance sheet as on 31st March, 2013 was as follows:

Balance Sheet as on 31st March, 2013

31st march, 2013

Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

Capital A/c |

| Furniture | 2,100 |

Akash | 50,000 | Stock | 28,700 |

Suraj | 50,000 | Land and Building | 35,000 |

General Reserve | 10,000 | Plant and Machinery | 49000 |

Sundry Creditors | 60,000 | Sundry debtors | 63,000 |

Bills Payable | 17,000 | Cash | 9,200 |

| 1,87,000 |

| 1,87,000 |

They agreed to admit Sanjay in their partnership on 1st April, 2013, on the following terms:

(1) Sanjay should bring Rs. 1,500, as his share of goodwill in the firm, and Rs. 2,000 as his capital.

(2) Reserve for doubtful debts is to be provided @ 5% on debtors.

(3) Land and building be depreciated at 10% p.a.

(4) Plant and Machinery to be depreciated @ 5% and stock to be depreciated @ 10% p.a.

(5) The new profit sharing ratio will be 2: 1: 1.

Prepare:

(a) Revaluation Account.

(b) Partners’ Capital Accounts.

(C) New Balance Sheet of the firm.

OR.

Given below is the balance sheet of Vaishali, Madhuri and Shobha, who were sharing profits and losses in the ratio of 3 : 3 : 2. [Solution] Balance Sheet as on 31st March, 2012

Liabilities | Amount (Rs. ) | Assets | Amount (Rs. ) |

Creditors | 34,800 | Cash | 21,600 |

Bills Payable | 8,800 | Machinery | 34,800 |

Capital A/c |

| Debtors | 50,000 |

Vaishali | 48,000 | Stock | 25,200 |

Madhuri | 52,000 | Furniture | 16,000 |

Shobha | 36,000 | Buildings | 48,000 |

Reserved Fund | 16,000 |

|

|

| 1,95,600 |

| 1,95,600 |

On 1st April, 2012 Shobha retired from the firm on the following terms:

(1) Assets be revalued as under:

Stock Rs. 24,000, Machinery Rs. 32,000, Furniture Rs. 16,800.

(2) R.D.D. be maintained at 4% on debtors.

(3) An item of Rs. 400 from creditors is no longer a liability and hence should be properly adjusted.

(4) The amount due to Shobha be transferred to her loan account.

Pass necessary Journal Entries in the books of the firm.

Q. 4. Ramesh sold goods to Ganesh on credit for Rs. 20,000. Ganesh accepted a bill of Rs. 20,000 for 3 months, drawn by Ramesh on the same date. [Solution] On the due date Ganesh dishonoured his acceptance. Then Ganesh approached Ramesh and requested for renewal of the bill.

Ramesh agreed on the condition that Ganesh should pay Rs. 10,000 in cash and accept a new bill for 2 months for the balance amount plus interest Rs. 200.

The new bill was drawn by Ramesh and accepted by Ganesh. However one month before the due date Ganesh retired his acceptance by paying Rs. 9,900.

Pass necessary Journal Entries in the books Ramesh.

Q5. Mr. Aaba and Mr. Baba are equal partners whose Balance Sheet as on 31st March, 2012 was as under: [10]

Balance Sheet as on 31st march, 2012

Liabilities | Amount (Rs. ) | Assets | Amount (Rs. ) |

Sundry creditors | 16,000 | Cash in hand | 500 |

Capital A/c |

| Stock | 4500 |

Aaba | 2000 | Debtors | 4000 |

Baba | 2000 | Plant and Machinery | 5000 |

|

| Furniture | 2000 |

|

| Land and building | 4000 |

| 20000 |

| 20000 |

Due to weak financial position of the partners the firm is dissolved. Aaba and Baba are not to contribute anything from their private estate, hence they are declared insolvent.

the assets are realised as follows:

Stock Rs. 3,000, Plant and Machinery Rs. 3,000. Furniture Rs. 1,000, Land and Building Rs. 2,000 and Debtors Rs. 500.

You are required to prepare necessary Ledger Accounts to close the books of the firm.

OR

Joshi - Patil Ltd. issued 2,000, 10% debentures of Rs. 100 each, payable Rs. 20 on application and the balance on allotment.

Company received applications for 2,500 debentures, out of which applications for 2,000 were allotted fully and remaining applications were rejected and the money refunded.

Journalise the above transactions, assuming that all the sums were received.

Q6. Following is the Balance Sheet and Receipts and Payments Account of the Sevagiri Hospital, Satara.

Prepare Income and Expenditure account for the year ended on 31st March, 2013 and Balance Sheet as on that date.

Balance sheet as on 1st April, 2012

Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

Capital Fund | 10,00,000 | Cash in hand | 6,000 |

Outstanding Salaries | 22,000 | Cash at bank | 30,000 |

Medical bill unpaid | 6,000 | Land and building | 8,00,000 |

|

| Furniture | 70,000 |

|

| Equipments | 1,20,000 |

|

| Outstanding subscription | 2,000 |

| 10,28,000 |

| 10,28,000 |

Receipts and Payments Account for the year ending 31.03.2013

Dr. |

|

| Cr. |

Receipts | Amount (Rs.) | Payments | Amount (Rs.) |

To Balance b/d |

| By Salaries

[including of previous year] | 1,10,000 |

Cash in hand | 6000 | By Medicines | 48,000 |

Cash at bank | 30,000 | By Equipment purchased | 20,000 |

To Subscription [includes 2000 received for previous year] | 1,30,000 | By Taxes | 3000 |

To Sale of old furniture [book value Rs. 30,000] | 20,000 | By General Expenses | 8600 |

To Donations [revenue] | 44,000 | By Balance c/d |

|

To Life membership fees | 25,000 | Cash in hand | 15,400 |

|

| Cash at bank | 50,000 |

| 2,55,000 |

| 2,55,000 |

Consider the following adjustments:

(1) Outstanding subscription Rs. 15,000

(2) Capitalise the amount of life membership fees.

(3) Pre - paid taxes RS. 500.

(4) Outstanding salary Rs. 12,000.

(5) Write off depreciation RS. 20,000 from land and building and Rs. 30,000 from equipments.

(6) Outstanding medicine bill as on 01.04.2012 is still due.

Q7. From the following Trial Balance of M/s Sanjay and Keshav, you are required to prepare Trading and Profit and Loss Account, for the year ended 31st March 2013 and Balance Sheet as on that date after taking into account the following additional information.

Trial Balance as on 31st March, 2013

Debit Balances | Amount (Rs.) | Credit Balances | Amount (Rs.) |

Opening Stock | 1,80,000 | Sales | 5,25,000 |

Bills receivable | 80,000 | Rent | 22,000 |

Purchases | 240000 | Bills Payable | 78000 |

Bad debts | 20000 | Sundry creditors | 100000 |

Salary and Wages | 24000 | Capital Account |

|

Discount | 9,000 | Sanjay | 5,00,000 |

Carriage inward | 12,000 | Keshav | 3,00,000 |

Travelling expenses | 13,000 |

|

|

Cash in hand | 38,000 |

|

|

Furniture | 2,80,000 |

|

|

Insurance | 12,000 |

|

|

Land and Building | 4,00,000 |

|

|

Postage and telegram | 7,000 |

|

|

Sundry debtors | 2,10,000 |

|

|

| 15,25,000 |

| 15,25,000 |

Additional Information:

(1) Insurance paid in advance Rs. 3,000.

(2) Depreciation provided on furniture at 10%.

(3) Salary and wages outstanding Rs. 6,000.

(4) Rent received in advance Rs. 5,000.

(5) Closing stock as on 31.03.2013 Rs. 2,00,000.

**********************************************************************************