HSC ACCOUNTS MARCH 2017 SOLUTION

1. A. (i) Statement of Profit or Loss is prepared under the Single Entry System to ascertain profit.

(ii) The debit balance of insolvent partner’s capital account which insolvent partner cannot pay is called capital deficiency.

(iii) Non - recurring expences are those capital expenses which are spent for acquisition of fixed asssets like purchase of land or furniture, in order to run the concern and it gives benefits for a lon period say more than 3 years.

(iv) Gain ratio is calculated at the time of retirement of a partner by deducting old ratio from new ratio.

(v) A bill of exchange is said to be retired if its acceptor makes payment of it before its due date, usually after deducting some discount or rebate.

Q1. B.

(i) Bad debts

(ii) Drawee

(iii) Gross Profit ratio / Turnover ratio.

(iv) Dissolution of Partnership firm.

(v) Notary Public.

Q. 1. C.

(i) Goodwill is an intangible asset.

(ii) Debenture is an acknowledgement of debt under common seal of a company.

(iii) Whem closing capital is greated than opening capital it is denotes Profit.

(iv) Cash proceeds from the issue of debentures is a Financial activity.

(v) Payee is a person to whom the amount on a bill is payable.

Q. 1. D.

(i) True

(ii) False

(iii) True

(iv) False

(v) False.

Q. 1. F.

2. In the books of Mr. John.

Statement of Affairs.

Liabilities

|

1.4.12

|

31.3.13

|

Assets

|

1.4.12

|

31.3.13

|

Sundry Creditors

|

54500

|

60400

|

Machinery

|

70000

|

70000

|

Capital Fund

(Balancing Figure)

|

178700

|

216400

|

Furniture

|

10000

|

20000

|

Stock

|

36000

|

42000

| |||

Sundry Dentors

|

72200

|

88400

| |||

Cash in Hand

|

3000

|

4100

| |||

Cash at Bank

|

42000

|

52300

| |||

233200

|

276800

|

233200

|

276800

|

Statement of profit or Loss for the year ended 31st March, 2013

Particulars

|

Amount

(Rs.)

|

Amount

(Rs.)

|

Capital at the endo fothe accounting year. 2012 - 13

|

216400

| |

Add: Drawings made duing the accounting year.

|

15000

| |

231400

| ||

Less: Additional Capital Introduced

|

20000

| |

Adjusted Closing Capital

|

211400

| |

Less: Capital at the begining of the accounting year

|

178700

| |

32700

| ||

Less: Depreciation

| ||

On Machinery (10% on Rs.70000 for 1 year)

|

7000

| |

On Opening Furniture (20% p.a. On Rs. 10000 for 1 year)

|

2000

| |

On Additional Furniture (20% on Rs. 10000 for 6 months)

|

1000

|

10000

|

Net profit Earnied during the year.

|

22700

|

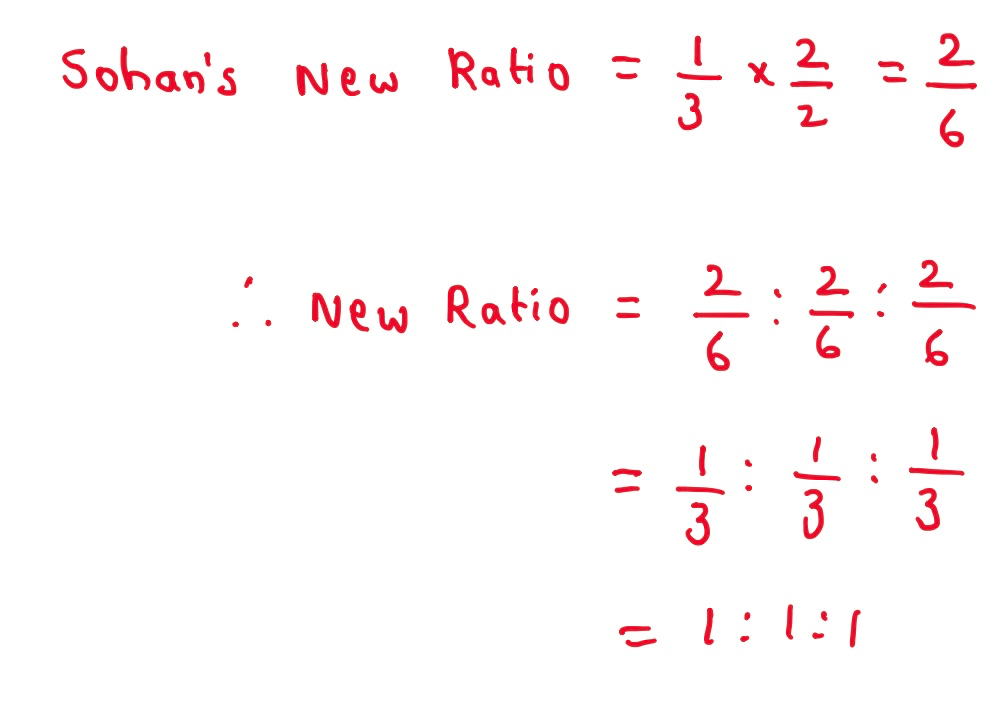

3. In the books of Partnership Firm

Profit and Loss Adjustment Account

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Furniture A/c

(Depreciation)

|

1500

|

By Stock A/c

(Appreciation in Value)

|

2500

| ||

To partners’ Capital Account.(Profit)

| |||||

Ram

|

500

| ||||

Madan

|

500

|

1000

| |||

2500

|

2500

|

Partners Capital Accounts

Particulars

|

Ram

|

Madan

|

Sohan

|

Particualrs

|

Ram

|

Madan

|

Sohan

|

To Goodwill A/c

|

10000

|

10000

|

10000

|

By Balance b/d

|

100000

|

100000

| |

By General Reserves A/c

|

20000

|

20000

|

-

| ||||

By Bank A/c

(Capital Contribution)

|

-

|

-

|

100000

| ||||

By Goodwill A/c

|

15000

|

15000

| |||||

By Profit & Loss Adj. A/c

(Profit)

|

500

|

500

| |||||

To Balance C/d

|

125500

|

125500

|

90000

| ||||

135500

|

135500

|

100000

|

135500

|

135500

|

100000

|

Balance Sheet as on 1st April, 2012

Liabilities

|

Amount

|

Amount

|

Assets

|

Amount

|

Amount

|

Sundry Creditors

|

55300

|

Plant & Machinery

|

90000

| ||

Partners’ Capital A/c

|

Furniture:

|

15000

| |||

Ram

|

125500

|

Less: Depreciation @10%

|

1500

|

13500

| |

Madan

|

125500

|

Sundry Debtors

|

91000

| ||

Sohan

|

90000

|

341000

|

Stock

|

68000

| |

Add: Increase in value

|

2500

|

70500

| |||

Cash in Hand

|

4200

| ||||

Cash at Bank

|

127100

| ||||

396300

|

396300

|

Goodwill A/c

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Ram’s Capital A/c

|

15000

|

By Ram’s Capital A/c

|

10000

| ||

To Madan’s Capital A/c

|

15000

|

By Madan’s Capital A/c

|

10000

| ||

By Shohan’s Capital A/c

|

10000

| ||||

30000

|

30000

|

Bank A/c

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Balance b/d

|

27100

| ||||

To Sohan’s Capital A/c

|

100000

|

By Balance C/d

|

127100

| ||

127100

|

127100

|

OR

3. Journal of Partnership Firm

Date

|

Particulars

|

L.F.

|

Debit (Rs.)

|

Credit (Rs. )

|

31.3.13

|

Reserve Fund A/c ..... Dr.

|

50000

| ||

To Sharmila’s Capital A/c

|

25000

| |||

To Urmila’s Capital A/c

|

15000

| |||

To Pramila’s Capital A/c

|

10000

| |||

[Being reserve fund distributed and transfrred to all partners’ capital account in their old ratio)

| ||||

31.3.13

|

Goodwill A/c ...... Dr.

|

12000

| ||

To Pramila’s Capital A/c

|

12000

| |||

[Being Goodwill raised and credited to Pramila’s Capital A/c ]

| ||||

31.3.13

|

Sharmila’s Capital A/c .... Dr.

|

7500

| ||

Urmila’s Capital A/c ..... Dr.

|

4500

| |||

To Goodwill A/c

|

12000

| |||

[Being Goodwill written off and debited to remaining partners’ capital A/c in their gain ratio]

| ||||

31.3.13

|

Land and Building A/c .... Dr.

|

20000

| ||

Stock A/c .... Dr.

|

2000

| |||

To Profit and Loss Adjustment A/c

|

22000

| |||

[Being appreciation in the value of Assets recorded]

| ||||

31.3.13

|

Profit and Loss Adjustment A/c .... Dr.

|

2000

| ||

To Furniture A/c

|

2000

| |||

[Being the furniture depreciated in value]

| ||||

31.3.13

|

Profit and Loss Adjustment A/c .... Dr.

|

20000

| ||

To Sharmila’s Capital A/c

|

10000

| |||

To Urmila’s Capital A/c

|

6000

| |||

To Pramila’s Capital A/c

|

4000

| |||

[Being profit on revaluation of assets and liabilities transfered to partners’ capital A/c ]

| ||||

31.3.13

|

Pramila’s Capital A/c .......Dr.

|

126000

| ||

To Pramila’s Loan A/c

|

126000

| |||

[Being balance due to Pramila transferred to her Loan A/c ]

|

Working Note: Profit and Loss Adjustment Account & Partners Capital Accounts

Profit and Loss Adjustment Account

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Furniture A/c

|

2000

|

By Land and Buildings A/c

|

20000

| ||

To Partners’ Capital A/c

|

By Stock A/c

|

2000

| |||

Sharmila

|

10000

| ||||

Urmila

|

6000

| ||||

Pramila

|

4000

|

20000

| |||

22000

|

22000

|

Partners Capital Accounts

Particulars

|

SHARMILA

|

URMILA

|

PRAMILA

|

Particualrs

|

SHARMILA

|

URMILA

|

PRAMILA

|

To Goodwill A/c

|

7500

|

4500

|

By Balance b/d

|

200000

|

150000

|

100000

| |

To Pramila’s Loan A/c

|

126000

|

By Reserve Fund

|

25000

|

15000

|

10000

| ||

By Goodwill A/c

|

-

|

-

|

12000

| ||||

By Profit & Loass Adjustment A/c

|

10000

|

6000

|

4000

| ||||

To Balance c/d

|

227500

|

166500

|

-

| ||||

235000

|

171000

|

126000

|

235000

|

171000

|

126000

|

4. Journal of Raja

Date

|

Particulars

|

L.F.

|

Debit (Rs.)

|

Credit (Rs. )

|

1

|

Cash/Bank A/c ... Dr.

|

10000

| ||

Pradhan’s A/c .... Dr.

|

30000

| |||

To Sales A/c

|

40000

| |||

[Being the goods sold and part payment received]

| ||||

2

|

Bills Receivable A/c ... Dr.

|

30000

| ||

To Pradhan’s A/c

|

30000

| |||

[Being the accptance received from Pradhan]

| ||||

3

|

Bills sent to Bank for Collection A/c ... Dr.

|

30000

| ||

To Bills Receivable A/c

|

30000

| |||

[Being the bill sent to the bank for collection]

| ||||

4

|

Pradhan’s A/c ... Dr.

|

30000

| ||

To Bill sent to Bank for Collection A/c

|

30000

| |||

[Being the bill is dishonoured]

| ||||

5

|

Cash/Bank A/c ... Dr.

|

15000

| ||

Bad debts A/c .... Dr.

|

15000

| |||

To Pradhan’s A/c

|

30000

| |||

[Being 50% of the amount due recovered from Pradhan]

|

In the Ledger of Raja

Pradhan’s Account

Date

|

Particulars

|

Amount

|

Date

|

Particulars

|

Amount

|

1.

|

To Sales A/c

[Credit Sales]

|

30000

|

2.

|

By Bills Receivable A/c

(Acceptance Received)

|

30000

|

4.

|

To Bill Sent to Bank for Collection A/c

(Bill sent to the bank)

|

30000

|

5.

|

By Cash / Bank A/c

[Amount recovered]

|

15000

|

5.

|

By Bad debts A/c

(Bad debts incurred)

|

15000

| |||

60000

|

60000

|

5. In the books of Partnership Firm

Realisation Account.

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Sundry Assets:

|

By Sundry Liabilities

(Sundry Creditors)

|

39700

| |||

Plant and Machinery A/c

|

40000

|

By R.D.D. A/c

|

1000

| ||

Furniture A/c

|

12000

|

By Bank A/c

| |||

Sundry Debtors A/c

|

61000

|

Plant and Macinery

|

30000

| ||

Stock A/c

|

28300

|

141300

|

Sundry Debtors

|

58000

|

88000

|

To Bank A/c

(Sundry Creditors)

|

38000

|

By Akbar’s Capital A/c

(Plant and Machinery)

|

10000

| ||

To Bank A/c

(Realisation Expenses)

|

2000

|

By Birbal’s Capital A/c

[Stock ]

|

27000

| ||

By Partners’ Capital A/c

| |||||

Akbar

|

9360

| ||||

Birbal

|

6240

|

15600

| |||

181300

|

181300

|

Partners’ Capital Accounts

Particulars

|

Akbar

|

Birbal

|

Particulars

|

Akbar

|

Birbal

|

To Realization A/c

(Assets taken over)

|

10000

|

27000

|

By Balace b/d

|

60000

|

40000

|

To Realisation A/c

(Loss)

|

9360

|

6240

|

By General Reserve A/c

[Transfer]

|

12000

|

8000

|

To Bank A/c

(Final Settlement)

|

52640

|

14760

| |||

72000

|

48000

|

72000

|

48000

|

Bank Account.

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Balance b/d

|

19400

|

By Realisation A/c

(Sundry Creditors)

|

38000

| ||

To Realisation A/c

(Assets Sold)

|

88000

|

By Realization A/c

(Expenses paid)

|

2000

| ||

By Akbar’s Capital A/c

[Final settlement]

|

52640

| ||||

By Birbal’s Capital A/c

[Final Settlement]

|

14760

| ||||

107400

|

107400

|

OR

5. Journal of Modern Chemicals Co. Ltd.

Date

|

Particulars

|

L.F.

|

Debit (Rs.)

|

Credit (Rs. )

|

1

|

Bank A/c ... Dr.

|

325000

| ||

To Equity Share Application A/c

|

325000

| |||

[Being share application money Rs. 5 per share received on 65000 shares]

| ||||

2

|

Equity Share Application A/c .... Dr

|

325000

| ||

To Equity Share Capital A/c

|

300000

| |||

To Bank A/c

|

25000

| |||

[Being application money transferred to share capital and excess appliation monery refunded. ]

| ||||

3

|

Equity Share Allotment A/c ....Dr

|

300000

| ||

To Equity Share Capital A/c

|

300000

| |||

[Being allotment money of Rs. 5 per share due on 60000 shares)

| ||||

4

|

Bank A/c ... Dr.

|

300000

| ||

To Equity Share Allotment A/c

|

300000

| |||

[Being allotment monery received]

| ||||

5

|

Equity Share First Call A/c .... Dr.

|

240000

| ||

To Equity Share Capital A/c

|

240000

| |||

[Being first call monery Rs. 4 per share due on 60000 shares)

| ||||

6.

|

Bank A/c .... Dr.

|

240000

| ||

To Equity Share First Call A/c

|

240000

| |||

[Being first call monery received]

| ||||

7

|

Equity Share second call A/c ... Dr.

|

180000

| ||

To Equity Share Capital A/c

|

180000

| |||

[Being second call money Rs. 3 per share due on 60000 shares]

| ||||

8

|

Bank A/c .... Dr.

|

179700

| ||

Equity Share Second call in Arrears A/c ... Dr.

|

300

| |||

To Equityu share Second call A/c

|

180000

| |||

[Being second call money received on all shares except 100 shares]

|

6. In the books of Adarsh Cultural Club, Mumbai

Income and Expenditure Account for the year ended 31st March, 2013

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Salaries

|

35300

|

By Subscriptions

|

48000

| ||

Less: Previous year’s Outstanding Salaries paid

|

1300

|

Add: Outstanding for current year

|

2000

|

50000

| |

Add: Outstanding for the current year.

|

700

|

34700

|

By Drama Receipts

|

28000

| |

To General Expenses

|

8400

|

Less: Drama Expenses

|

16000

|

12000

| |

To Printing & Stationery

|

4200

| ||||

To Depreciation on Furniture

|

5000

| ||||

To Excess of Income Over Expenditure (Surplus)

|

9700

| ||||

62000

|

62000

|

Balance Sheet as on 31st March, 213

Liabilities

|

Amount

|

Amount

|

Assets

|

Amount

|

Amount

|

Capital Fund

|

257000

|

Buildings

|

250000

| ||

Add: Surplus

|

9700

|

266700

|

Furniture

|

20000

| |

Building Fund

|

50000

|

Add: New Furniture Purchased

|

10000

| ||

Add: Donation for Building Fund

|

20000

|

70000

|

Less: Depreciation

|

5000

|

25000

|

Subscriptions received in advance

|

2000

|

Outstanding Subscription for 2012 - 13

|

2000

| ||

Outstanding salaries for 2012 - 13

|

700

|

Cash at Bank

|

57800

| ||

Cash in Hand

|

4600

| ||||

339400

|

339400

|

7. In the books of Partnership Firm of Jaya and Maya

Trading A/c For the year ended 31st March, 2011

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Opening Stock

|

32800

|

By Sales

|

194000

| ||

To Purchases

|

109000

|

By Closing Stock

|

22600

| ||

Less: Purchase of furniture wrongly included

|

10000

|

99000

| |||

To Carriage Inwards

|

3700

| ||||

To Wages and Salaries

|

28600

| ||||

To Gross Profit C/d

|

52500

| ||||

216600

|

216600

|

Profit & Loss Account for the year ended 31 st March, 2011

Particulars

|

Amount

|

Amount

|

Particulars

|

Amount

|

Amount

|

To Insurance

|

3700

|

By Gross Profit b/d

|

52500

| ||

To Rent, Rates and Taxes

|

14600

|

By Commission

|

5500

| ||

To Office Expenses

|

7300

| ||||

To R.B.D.D. A/c

| |||||

New Reserve

|

4400

| ||||

Less: Old Reserve

|

2000

|

2400

| |||

To Depreciation on Land and Building

|

30000

| ||||

Plant and Machinery

|

6000

|

By Partners’ Current A/c

[Net Loss]

| |||

Furniture

|

4000

|

40000

|

Jaya

|

4000

| |

Maya

|

6000

|

10000

| |||

68000

|

68000

|

Partners’ Current Accounts

Particulars

|

Jaya

|

Maya

|

Particulars

|

Jaya

|

Maya

|

To Drawings A/c

|

500

|

1500

|

By Balance b/d

|

3400

|

9100

|

To Profit & Loss A/c

|

4000

|

6000

|

By Balance b/d

|

1100

| |

To Balance c/d

|

1600

| ||||

4500

|

9100

|

4500

|

9100

|

Balance Sheet as on 31st March, 2013

Liabilities

|

Amount

|

Amount

|

Assets

|

Amount

|

Amount

|

Partners’ Capital A/c

|

Land and Building

|

300000

| |||

Capital A/c

|

Less: Depreciation

|

30000

|

270000

| ||

Jaya

|

200000

|

Plant and Machinery

|

60000

| ||

Maya

|

250000

|

450000

|

Less: Depreciation

|

6000

|

54000

|

Sundry Creditors

|

45600

|

Furniture

|

15000

| ||

Maya’s Current A/c

|

1600

|

Add: New furniture Purchased

|

10000

| ||

Less: Depreciation

|

-4000

|

21000

| |||

Sundry Debtors

|

88000

| ||||

Less: R.D.D. @ 5%

|

-4400

|

83600

| |||

Closing Stock

|

22600

| ||||

Cash in Hand

|

4700

| ||||

Cash at Bank

|

40200

| ||||

Jaya’s Current A/c

|

1100

| ||||

497200

|

497200

|